Financial planning doesn’t have to be difficult; in fact, it’s simple to create a financial plan. Yes, there is a lot of technical jargon and complicated things we financial planners do behind the scenes, but many of those processes can be listed out in layman’s terms. What if we told you that you could set up a thorough financial plan with or without a financial planner?

We are fortunate to be able to call some of the best and brightest minds in medicine our clients. However, it seems like every time they sit down in the hospital cafeteria, they come to us with some new or interesting idea that they heard from their other doctor friend. It goes something like this: “Hey Chad, I had lunch with Dr. Smith today, and he told me about this great life insurance plan that acts like a pension but with no downside risk.” Or something like, “I grabbed coffee with Dr. Thomas yesterday, and she said I should invest in her friend’s new small business — they are going to be the next Amazon!”

Now, while both those statements could be true, we often over-complicate our financial lives and believe it is the next big idea. While it is nice to dream about the next Amazon stock idea or the perfect “riskless” investment solution, the reality is that there are no quick fixes or get-rich-quick financial planning ideas with high probability. In personal finance, there is no replacement for hard work and long-term savings.

The biggest factor in your future riches is how much you save today. And while saving is a huge part of the equation, you also have to make sure the proper risk management is in place. Hopefully, you stay healthy and can work as planned for your entire career, but if you have any type of long-term disability, it can be nearly impossible to make your plan work. The same goes for any large lawsuit.

Prefer video over the blog? We’ve got you covered! Watch our YouTube video as we dissect this blog post for you.

KEY TAKEAWAYS:

- Tracking your cash flow and budget sounds boring, but it’s one of the best ways to ensure your finances match your priorities. It’ll also help you pay off your credit card debt and start an emergency fund.

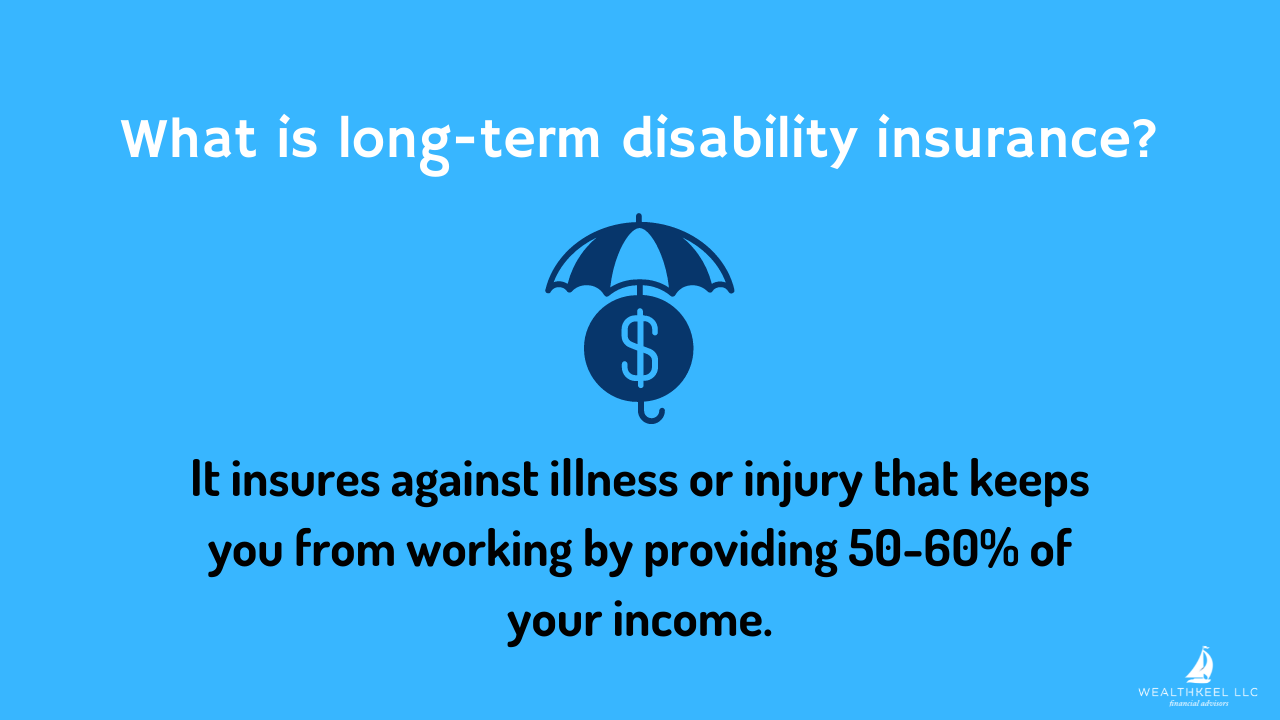

- Long-term disability insurance and term life insurance are essential to provide options in the event you can’t work.

- Maximize your employer’s retirement plan and tax-advantaged savings accounts to take advantage of the 8th wonder of the world: compounding interest!

- Create a game plan for your debt to stay on track with your building blocks for a solid financial foundation.

Now, let’s get started with 9 straightforward ways to help build a solid financial plan today, and into the future, with or without a financial planner. These are just about in order of significance as well, but you could switch a few around depending on your unique situation.

1) Track Your Cash Flow and Budget

Budgets can feel rather mundane and boring — we get it. However, having a monthly budget and consistently tracking your cash flow is the basis and solid foundation of any financial plan. You need to see the money coming in and the money going out, and usually, the money goes out a lot faster than you originally thought. You have to tell your money where to go, and if you don’t, your money will go to bad places (Amazon “one-click”, those “must-have” heels, and that “can’t miss” sporting event).

When making your monthly budget, you have to account for recurring expenses such as:

- Rent/mortgage

- Utilities

- Groceries

- Car payments

- Savings/retirement account contributions

- Gym memberships

- Cell phone bill

The list goes on, but you get the picture. You’ll also have to put away a percentage of your paycheck toward an emergency fund, just in case something unexpected happens, as well as long-term savings. There are many recurring monthly expenses that you need to account for.

There are also miscellaneous, low-priority but high-cost expenses such as:

- Subscriptions like Spotify, Netflix, Hulu, BarkBox, etc.

- Eating out/take out

- Entertainment, concerts, etc.

- Cable

- Clothing, jewelry, and other shopping expenses

These types of expenses may seem small or inexpensive — but $15 for Netflix, $20 for lunch 3 days a week, and the $12 Hulu subscription for that one show you like, and you’re already at $267 for the month. It all adds up incredibly quickly.

Creating a budget is as easy as opening up an Excel Spreadsheet or Google Sheets and putting in numbers. There are also some online tools available such as Tiller & YNAB. It doesn’t matter what you use — as long as you know how much money is coming in and going out each month, you’re in good shape.

2) Pay Your Credit Cards Off in Full Each Month

I’ll say it again: pay your credit cards off in full each month. Even with the best credit score, your interest rate is probably around the ballpark of 15%, but the average interest rate is anywhere from 16-22%. When you don’t pay your credit card bill on time, you’re subject to late fees, increased interest rates, and a serious demotion to your credit score.

Your credit score comes into play when you need a loan, want to rent an apartment, need insurance, or want a different credit card. Once your credit score is at 700, you’re considered a low/minimal risk. But once you have a late payment on your credit card, you can lose up to 110 points off of your credit score — and that takes a long time to get back.

When we see clients struggle with credit card debt, we usually switch them over to a cash budget. Credit card swipes are painless, and it is easy to use them with no remorse. However, handing cash over has a different emotional connection. This is why the envelope system from Dave Ramsey can be so powerful — cash has a deep emotional connection to us. If you can’t pay your credit cards off each month, try using cash for a few months for discretionary spending.

Good Tools: You and your willpower; there’s no app for this.

3) Fund Your Emergency Fund

We can’t stress this enough — your emergency fund is vital. It comes up in nearly every article we write. If your car stopped running and you needed a new engine, would you be able to fund that? If you were out of work for a couple of months, would you be able to make it? This is when your emergency fund kicks into high gear. It’s for those moments that you never saw coming.

Many get overwhelmed when they see these large goals for emergency funds, but it’s all about starting slowly.

In a perfect world, you should have 3 to 6 months of your total expenses saved away for your emergency fund. We use $20,000 as a starting goal, but we know you won’t get there immediately. So start with a small goal of $1,000 by using an auto-savings for $200 per paycheck and continue to grow your emergency fund.

Good tools: Set an auto-deposit directly to your emergency fund so you’re not tempted to use that money for other things. Your emergency fund should be a separate account, away from your traditional savings or checking account.

4) Long-Term Disability Insurance

Why? Long-term disability insurance is meant to insure against an injury or illness that will keep you out of work for a long duration of time. This is completely different from a worker’s comp type issue, so it’s important not to confuse the two. Long-term disability insurance gives you options for income beyond your established emergency fund.

1 out of 4 of us will face a long-term disability event, and the top 4 claims are musculoskeletal, cancer, injuries, and then cardiovascular. According to the Social Security Administration, 1 in 4 of today’s 20-year-olds will be disabled at some point in their lives before they reach 67, so this is something to take seriously.

If you become disabled because of an accident, injury, or illness, long-term disability insurance will typically pay 50-60% (maybe up to 70%) of your income while you’re not able to work. If the benefits come from a private policy, the benefits are paid tax-free, hence the reason why they only insure 50-60% of your income — it avoids moral hazard for you getting paid more while you are disabled vs. working.

Good tools: Your best place to start is with your employer — most employers will offer a group long-term disability option. Now, it may not be the world’s best coverage, but it is better than nothing. After that, get a few quotes via a private policy.

5) Term Life Insurance

If you are single and no one relies on your income or no one is responsible for your student loan debt (ex: co-signer on student loans), then you may not need life insurance just yet. However, even if you are young and healthy, it may still be a good idea to lock in a low-cost term policy. Just about everyone should have some form of life insurance.

Term life insurance is very inexpensive — for a great policy, you can expect to pay no more than $100 a month. A good starting place for most people is a $1,000,000 to $2,000,000 policy. As your income increases, you can add additional term life insurance as needed.

When you’re looking for a term life insurance policy, work with a company with a 90+ or higher Comdex score to ensure credibility. Also, if you’re in a single-income household and/or have a low emergency fund, add a waiver of premium for security.

Good tools: You probably have the option to add some group term insurance from your employer, which is a good starting place. A group policy can be good for some and bad for others. If you have had some health issues in the past, your group plan could be much lower cost than a private plan, because you are being “grouped” with other employees to spread out your risk.

However, if you are healthy and can obtain a good health rating, a private policy may be a lower cost. Moral of the story: shop around, get a few quotes from private insurers, and review the cost of your group plan. Here are a few more details on what to look for.

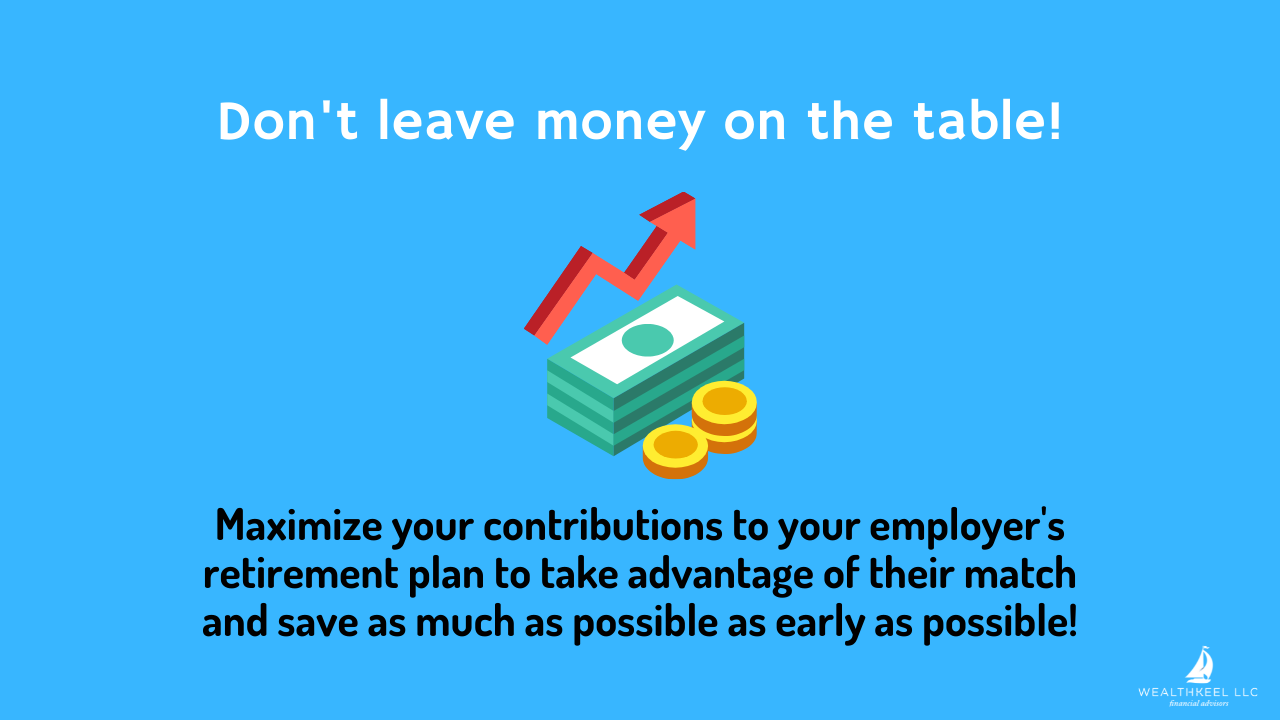

6) Maximize Your Employer Retirement Plan

Many employers offer a 401k, 403b, and/or some type of qualified plan. Take every advantage of it! Hopefully, they offer a match of some sort, but even if they don’t, this is the easiest way to get started on saving for retirement. We’ve said it before and we will say it again: start saving for retirement as early as possible. The worst that could happen is that you could retire earlier or have “too much” money in retirement!

If you are under the age of 50, you can save up $23,000/year (2024) for your retirement account. If you are older than 50, you can “catch up” toward your retirement savings goal and save up to $30,500. We won’t dig into the tax advantages or the Roth option to keep this simple, but at the end of the day, just save as much as you can as early as possible!

Good tools: Your employer’s retirement plan. Don’t be afraid to ask HR for more details. It’s easy to get overwhelmed with the many different investment options, but there should be a 401k representative to help you. Worst-case scenario: you pick a target-date fund that coincides with your estimated retirement year.

Bonus points: See if you have access to a 457b plan!

7) Maximize Your Other Tax-Advantaged Savings Plans

If the bucket above (employer retirement plan) is filled to the brim, then look to save another $7,000 or $8,000 if you are age 50+ (2024) into a traditional IRA or Roth IRA (Backdoor Roth IRA*). With a traditional IRA, you can contribute pre- or post-tax dollars, but your money will be taxed at your ordinary income rate after age 59 ½. With a Roth IRA, you can contribute post-tax dollars and your money will grow tax-free. You can make qualified tax-free withdrawals from your Roth after age 59 ½.

*For our physicians, your income is likely too high to be able to use an IRA and/or Roth IRA outright; you likely need to use a Backdoor Roth IRA.

Good tools: While the investing world can seem daunting, it is actually very easy to set up an account at places such as Fidelity, Vanguard, or TD and open an IRA/Roth IRA. Again, don’t get overwhelmed by the investment options. If you don’t want to put in the research to build a diversified portfolio, pick a target date fund that coincides with your estimated retirement year or desired risk tolerance.

8) Save Enough to Taxable Investment Accounts to Help Accomplish Other Goals (Ex: Early Retirement, Vacation Home, Etc.)

Truthfully, if you just filled the two buckets above, you would be way further than many of your peers. However, if your goal is financial independence and the opportunity to retire early, then you will have to be more aggressive with your savings. Now would be the time to open a taxable account for excess savings.

Taxable accounts tend to offer more flexibility than 401ks, IRAs, and/or 529 plans. With a taxable account, there are no minimum required distributions, you can take advantage of tax-loss harvesting, and you can use that money for anything you want at any time, with no penalties. As a friendly reminder, Uncle Sam always gets his cuts, so if there are gains, you would be subject to capital gains tax.

Good tools: The easiest way to do this is to open a taxable account (individual or joint) at the same custodian as your IRA/Roth IRA. Most custodians have allocation tools you can use for suggested allocations — here is an example from Vanguard. So if you are sick of target-date funds, this can show you an allocation suggestion based on your responses.

9) Debt Game Plan

Hopefully, all your debt is paid down and you no longer have to worry about student loans or Public Service Loan Forgiveness. If you do still have some student debt straggling along, it is vital to have a strategy in place to pay it off. Pay off as much as you can each month, even if that means you can’t go out for drinks one night — being debt-free is worth it.

If you no longer have student loans to worry about, start to pay down other debts more aggressively. A good rule of thumb is to start with the debt that incurs the highest interest rate first because the longer you don’t pay it off, the more expensive it’ll be.

Once all other debt is paid off, you may start to pay more on your mortgage principal each month; however, make sure you are on track for your investing goals first. Remember, the most powerful tool in finance is compounding interest, which is just time in the market.

Good tools: Follow your debt strategy as closely as possible. If you fall behind one month, pay off a little more the next month. Also, don’t forget about your budget — it’s there for a reason. If you need some help making a budget that best fits your lifestyle, refer back to the tools in the first bucket.

It’s as Simple as That

This is not a precise or completed financial plan by any means, but if we met you at age 30 and you said, “Chad, I don’t like you or WealthKeel,” but you followed these steps up until retirement, and we met again at age 50, we think you would be in a pretty good place.

If you followed these 9 steps, you would be tracking your cash flow to make sure there are no holes in the ship, you would have a fully-funded emergency fund, your risk management would be in good order with a disability and life insurance policy in place, you would have maxed out a 401k/403b and Backdoor Roth IRA for the past 20 years, and maybe even started a taxable account. More importantly, you would have no debt besides a mortgage.

Use these 9 steps as the building blocks toward a solid financial foundation. Go get ’em!

Looking for a more thorough, all-in-one spot for your financial life? Check out our free eBook: A Doctor’s Prescription to Comprehensive Financial Wellness [Yes, it will ask for your email 😉]