The “Backdoor Roth IRA” is a fantastic and commonly utilized Roth IRA strategy for physicians, but did you know there are other great ways to use a Roth IRA? Today, we are going to take a look at some other great Roth IRA strategies for physicians. 🎉

KEY TAKEAWAYS

- Roth IRAs offer unique benefits to investors because they are a source of tax-free distributions in retirement.

- While it’s generally recommended to avoid touching your Roth IRA for as long as possible, there are various strategies you can use to maximize utility throughout your career.

- These strategies include using a Roth IRA as a savings account, reducing taxable accounts, and providing relief for early retirees.

Prefer video over the blog? We’ve got you covered! Watch our YouTube video as we dissect this blog post for you:

What is a Roth IRA?

Roth IRAs are a powerful savings tool.

Unlike traditional IRAs, Roth IRAs are composed of post-tax contributions, which means that investors can make tax-free withdrawals in retirement. As such, Roth IRAs are a popular investment vehicle for individuals who may be at a higher tax bracket in retirement.

Roth IRAs are often considered to be the last investments investors should draw on in retirement.

Why?

They’re an excellent vehicle for long-term, tax-free, compounding growth, and they are one of the best (if not the best) assets to leave behind for inheritance purposes. That said, there are various unique strategies that savvy investors can use to maximize the utility of their Roth accounts both before and during retirement.

Roth IRAs come with contribution eligibility limits based on income, and many practicing physicians may run into these limits.

However, if your income is above the limit, there are still ways to take advantage of Roth IRAs through Backdoor Roth IRA contributions and Roth conversions. This means that Roth IRAs can still be a unique savings tool even for those who exceed the income limit for regular contributions.

Roth IRA Basics

- Roth IRAs are funded with after-tax dollars and feature compounding growth and tax-free withdrawals.

- In 2025, the maximum savings amount per year is $7,000 if you’re younger than 50 and $8,000 if you’re 50 or older.

- In 2025, your income must be less than $150,000 if you file your tax return as single and less than $236,000 if you’re married and filing jointly for full contributions.

- You can still save money in a Roth IRA if your income is above those levels, but the amount you can contribute is gradually phased out. Once your modified adjusted gross income reaches $165,000 filing single and $246,000 married filing jointly, you’re ineligible for direct contributions.

Source: Internal Revenue Service (IRS)

Roth IRA Strategies for Physicians

Here are some unique ways physicians can take advantage of a Roth IRA’s many benefits.

1. A Savings Tool for Young Investors

Most experts recommend that individuals have an emergency fund containing three to six months’ worth of expenses stashed away in a savings account before they start investing.

But try applying that advice to a young physician whose hundreds of thousands of dollars in debt and working on getting their bearings in the medical field.

Following such advice could mean that young people may have to wait months or even years while building up a safety net before they begin to invest seriously.

Luckily, this doesn’t always have to be the case.

By opening a Roth IRA, young physicians can use this type of account as a de facto savings tool while also kick-starting their retirement savings. Win-win!

Because Roth IRAs are composed of post-tax savings, investors can withdraw contributions from the account without penalty, making this type of retirement account a great savings vehicle even for investors who don’t yet have a robust emergency fund.

Keep in mind that while you can withdraw contributions from a Roth IRA tax-free, you can’t withdraw earnings tax-free. To keep it simple: you can only take out what you put in.

Pro-Tip: This assumes you are making direct contributions to a Roth IRA, aka not doing Backdoor Roth IRAs. Backdoor Roth IRAs are considered a conversion which then introduces the 5-year rule. Due to this fact, this strategy is best for medical students and/or residents/fellows that are under the income limits for direct contributions to a Roth IRA still.

If you end up needing the money, you can withdraw it from your account when you need it. At the same time, you can start saving for retirement much earlier than you would if you waited to build up a robust emergency fund in a traditional savings account—where yields will likely fall well short of inflation.

Pro-Tip: While I love this idea, try your best not to dip into these Roth IRA funds and instead work on establishing an Emergency Fund.

2. A Practice Owner/Small Business Opportunity

Roth IRAs may also be an attractive investment option for physicians that own their practice.

Under the Tax Cuts and Jobs Act, business owners can take a qualified business income deduction (QBI – sometimes called the 199A) on their personal income tax return. This presents unique opportunities for retirement savings since pre-tax contributions might be taxed at a higher rate when withdrawn in retirement.

Because of this deduction, it often makes sense to invest more heavily in post-tax retirement accounts like a Roth 401k instead of solely funding retirement accounts like 401(k)s with all pre-tax funds. Business owners can also execute Roth conversions to increase their taxable income and fully utilize this deduction.

I know, it sounds cool, and it is, but be sure you discuss this strategy with your accountant. There are phaseouts to qualify for the QBI deduction, making it essential to create a balanced retirement savings strategy.

3. An Avenue To Prioritize Tax-Free Withdrawals

Another investment strategy worth considering is transferring funds from taxable brokerage accounts into Roth accounts via contributions or conversions.

Why should physicians consider this course of action?

Many physicians are high-earners, and their salaries are projected to grow throughout their careers. This growth could leave their nest egg susceptible to higher taxes, especially in the event of potential future tax-law changes.

Employing a strategy to lower activity in taxable accounts is all about maximizing a physician’s tax-free withdrawals. It takes advantage of the tax-free nature of Roth IRAs.

Pro-Tip: I see this best used later in a physician’s career where we need to work on balancing their pre-tax with Roth assets. During their attending years, they likely accumulated a large amount in taxable accounts. Ideally, there are a few “golden” tax years between retirement and RMDs where their tax brackets are low. So, we will “fill their tax brackets” to a certain point. By converting pre-tax assets to Roth, we are going to create a tax bill. We then use the taxable account to fund that tax bill. Now, be careful about how you liquidate from your taxable account. In a perfect world, you are selling losers (tax-loss harvesting bonus!) or positions with a very low gain to pay the tax bill. The name of the game is to pay less in taxes today.

When you move money away from traditional pre-tax and brokerage accounts, you in turn reduce overall taxable income on personal returns. It’s easy to see how such actions actively minimize the risk of higher taxes in retirement.

By paying the tax up-front, ideally at a lower rate than in the future, physicians can insulate their retirement investments if they are in a higher tax bracket or if tax laws change.

4. A Path for Education Investing or Extra Savings for Your Kid(s)

Most parents are aware that they can save for their children’s education using tax-advantaged 529 plans.

Many 529 plans offer tax deductions for regular contributions up to a specific limit. But once that limit is reached, a 529 plan may not actually be the best place to stash funds meant for your child’s college tuition. Consider funding a 529 plan up to the amount covered by the state tax benefit and then contributing to a post-tax retirement account like a Roth IRA.

As a physician, your best route is if your child has earned income, and then you can open a Roth IRA for them and fund that investment for them. I would not “waste” your Backdoor Roth IRA each year on this strategy. Those are precious dollars each year.

Pro-Tip: If your child has earned income in a given year, consider funding a Roth IRA for them. Think of it as a match from the Bank of Mom or Dad.

Yes, Roth IRAs can be tapped for more than emergencies and retirement; distributions for qualified education expenses avoid the early 10% withdrawal penalty.

As with any Roth distributions before 59 ½, you will still have to pay income tax on the earnings portion of the withdrawal—a bit of a bummer. If you use a Roth IRA withdrawal for qualified education expenses, you can avoid the 10% penalty, but you will still owe income tax on the earnings portion. Most are surprised to hear this, but remember that your Roth IRA account balance is made up of contributions and earnings. You can always withdraw the contributions tax-free and penalty-free at any time, for any reason, because you have already paid tax on that income. However, you need to keep an eye on the earnings portion.

While current account balances in retirement accounts (401k, Roth IRA, etc.) aren’t counted on the FAFSA form, distributions from those retirement accounts are. So, if you take out $13,000 from a Roth IRA to pay for tuition, that $13,000 will show up as income on next year’s financial aid statement, which could jeopardize eligibility. To be frank, as a physician, your kid(s) are likely not getting financial aid. I hope I am not the first one to break this to you, but the FAFSA is likely not a deal-breaker.

5. Providing a Safety Net for Physicians Who Dream of Early Retirement

If you retire early, as some physicians intend to do, chances are you’ll face some unique challenges when it comes to retirement income, healthcare, and more. For example, many early retirees need to buy individual health insurance on the marketplace, assuming they are not yet old enough to qualify for Medicare (age 65).

Despite having to shoulder some of the costs traditionally associated with retirement, however, early retirees cannot touch many traditional sources of retirement income.

They may not yet have access to Social Security benefits, for example, and may not be able to draw on retirement accounts like traditional IRAs and 401k/403b without incurring a penalty (before age 59.5). However, there are some strategies for early retirees accessing funds from their 401k/403b and other qualified funds—age 55 rule & 72T rule. Review your plan with your advisor to understand the options available to you.

Because Roth qualified distributions do not count as income for the purposes of health insurance premium tax credits, early retirees can use Roth distributions to provide cash flow while also taking advantage of lucrative tax credits on their health insurance premiums.

This approach has the potential to save retirees thousands of dollars on healthcare expenses before they hit Medicare age. Early retirees can also use Roth accounts to supplement income until they can access other sources of retirement funds.

6. Avoiding Tax Dark Horses like IRMAA and Net Investment Income Tax

The Medicare Income-Related Monthly Adjustment Amount, also known as IRMAA, is the amount you have to pay in addition to your Medicare Part B premium if your income crosses certain thresholds.

Once you make above $106,000 filing single or $212,000 married filing jointly (2025 limits, based on 2023 MAGI), IRMAA should be top of mind. This can result in income “cliffs” where policy costs increase dramatically after only a slight increase in income—as little as $1.

Physicians need to carefully monitor their taxable income as it can create a domino effect of other taxes like IRMAA as well as net investment income tax, among others.

Net investment income tax is a 3.8% tax if your investments (interest, dividends, capital gains, rental income, etc.) exceed federal limits—$200,000 if filing single and $250,000 if married filing jointly (2025 limits).

Proper tax planning throughout the year works to minimize the impacts of these added tax burdens and unpleasant April surprises.

Using Roth distributions to supplement your other income can help to keep your overall income level low for the purpose of healthcare premiums and other taxable events. Since Roth withdrawals are post-tax, they don’t count as sources of taxable income.

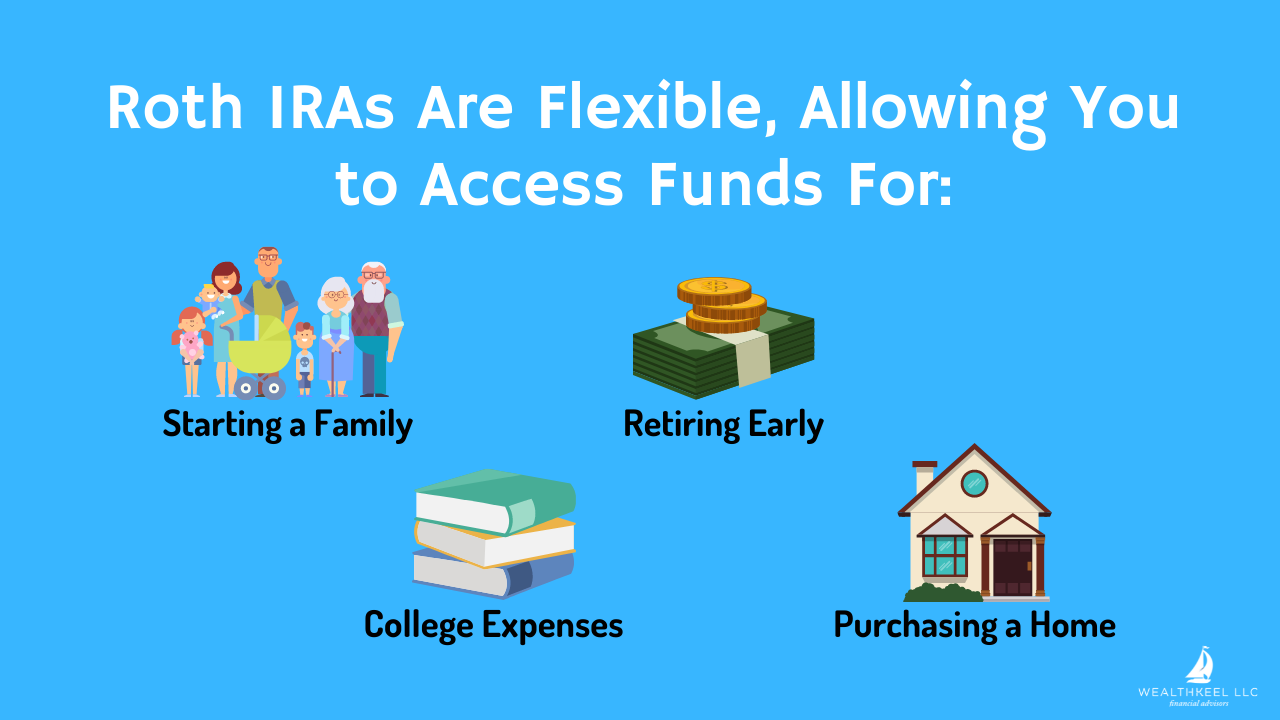

7. Extra Flexibility

Your Roth IRA offers unique flexibility in terms of access. With your Roth IRA, you will always have full access (tax & penalty-free) to the amount you contributed (again, conversions from a Backdoor Roth IRA have the 5-year rule each time). This means that you can take contributions out at any time, providing flexibility whether you plan to retire early or need to cover a significant expense.

You can also access funds for a qualified first-time home purchase and college expenses, even starting a family via birth or adoption expenses, thanks to the SECURE Act.

It’s essential to remember that the rules for withdrawing gains from your Roth IRA are different. To withdraw gains, two things must be true:

- You’ve had the account open and active for at least five years;

- You’re either over 59 ½, had a disability, or have passed away and given the account to a beneficiary.

A non-qualified distribution of gains may be subject to taxation of the earnings and a 10% penalty—which could put a damper on your cash flow.

Remember, your Roth IRA is, first and foremost, a retirement account. While there are a myriad of other benefits, you should avoid spontaneous or unplanned withdrawals. After all, you want to have some tax-free money to play with in your golden years!

8. An Estate Planning Tool

A Roth IRA can also be a fantastic estate planning tool and help you preserve your savings for the next generation.

Since there are no required minimum distributions, you can continue growing the account balance during retirement and only withdraw funds when needed.

Because taxes have already been paid in advance, the accounts are also subject to tax-deferred and compounding growth. Roth IRA assets also avoid probate as long as you have designated beneficiaries.

Keep in mind that most non-spouse beneficiaries will need to withdraw the account’s entire balance within ten years thanks to the elimination of the Stretch IRA from the Secure Act.

With all of these combined benefits, Roth IRAs are a helpful estate planning tool for many retirees.

Roth IRAs for Gen X and Gen Y Physicians

Roth IRAs are an excellent retirement savings vehicle for Gen X and Gen Y doctors.

In a Nutshell

- Tax-free source of retirement income

- Take advantage of a lower tax bracket now

- Have more flexibility in retirement

Why should Gen X & Gen Y use a Roth IRA? One of the main advantages of contributing to a Roth IRA is that you lock in a present-day tax rate. Your post-tax contributions are free to grow over time, and you won’t have to pay taxes on these savings in retirement.

This can be especially helpful for higher earners who may want to take advantage of low current tax rates. While there’s no predicting the future, tax rates may likely increase over time. Roth IRAs allow you to pay taxes today when you know what your tax rate is, take advantage of tax-deferred compounding growth for a few decades, and then enjoy your money tax-free in retirement.

Some Gen X and Gen Y physicians may mistakenly believe that their tax bracket will be lower in retirement. After all, they won’t be working any longer, so they might assume that their income will be less as a result. However, this doesn’t take into account the many different sources of retirement income.

While their parents and grandparents could retire off of their Social Security and pension incomes, Gen X & Gen Y are less able to rely on guaranteed sources of income in retirement.

Instead, they must rely on retirement savings in the form of 401ks/403bs and IRAs. Withdrawals from traditional retirement savings accounts count as a source of taxable income, which can raise your income tax during retirement. In addition, many retirees may not want to reduce their expenses in retirement.

If taxes have gone up, the case for the Roth IRA is even more compelling. Because Roth IRA qualified withdrawals are not taxable, you’ll have a guaranteed source of tax-free income in retirement, regardless of what the tax rate is.

Roth IRAs for Baby Boomer Physicians

If you’re nearing retirement, the advantages of a Roth IRA may not be quite as straightforward, but there are still plenty of benefits to strategically using a Roth IRA.

In a Nutshell

- Bypass required minimum distribution (RMD) rules

- Lower sources of taxable income in retirement

- Preserve retirement savings for the future

One of the main ways baby boomer physicians can use Roth IRAs is to bypass RMDs and continue to grow their savings even after they retire.

Baby boomer physicians may have both pension and social security income streams, as well as an extensive portfolio of assets. In some cases, these retirees may be able to maintain their current lifestyle with funds from just their pension and social security income. While they might withdraw money from retirement accounts for a trip or a unique occasion, they may not need to consistently withdraw money from retirement accounts.

However, once baby boomer physicians turn 73 or 75 (depending on their birth year), they need to take required minimum distributions (RMDs) from their traditional retirement accounts. If you don’t take a required minimum distribution, you’ll be taxed 25% on the RMD amount—ouch!

For example, let’s assume you were living comfortably off of $84,000 per year ($7,000/m) in retirement, and you now have $1,000,000 in IRA assets at age 75. Even though you don’t need any more income for this year, the government will require you to take minimum required distributions. You would be required to withdraw $40,650 (or pay a $10,163 penalty). That $40,650 is added to your income and taxed at your current income tax bracket.

$1,000,000/24.6 (2025 RMD Table, age 75) = $40,650

Luckily, Roth IRAs don’t require an RMD, so the above scenario can be eliminated or at least limited. Most boomers have a few decades of a head start on 401k/403b and traditional IRA savings, so getting to an equal split between traditional retirement accounts and Roth assets would be difficult. That said, it’s a good idea to start saving to a Roth IRA or even a Roth 401k heading into retirement to try to add flexibility to your retirement withdrawal options.

Pro-Tip: Take advantage of bad market years and convert some pre-tax to Roth inside of your accounts. Also, take advantage of lower tax bracket years to convert pre-tax to Roth.

Conclusion

Roth IRAs are a fantastic investment vehicle (personally, they are my favorite), no matter your age. Because they are composed of post-tax contributions, they offer unique tax advantages, especially for high-income individuals who expect that their tax rate will be even higher in retirement than it is currently. They’re also a great complement to pre-tax retirement accounts like traditional IRAs and 401k/403bs, as well as other tax brokerage accounts.

While you can use your Roth IRA as a straightforward retirement account, there are some unique strategies for maximizing your Roth IRA’s potential under certain circumstances. Depending on your age and financial situation, this can include doubling as a savings account, lowering your health insurance premiums before and during retirement, or reducing your tax burden after you retire.

Looking for a more thorough all-in-one spot for your financial life? Check out of free eBook, A Doctor’s Prescription to Comprehensive Financial Wellness.