Whether you are a resident or fellow, I am sure you know how essential insurance is for you. The problem is that you may not be sure of what coverage you need or how much. Let’s face it; insurance can sometimes feel like its own little world. Have no fear, this post will cover insurance 101 for physicians in training! The other title we were going to use was, “If they say Northwestern Mutual, RUN!” 😂

Who really wants to shell out hundreds of dollars for a situation that (hopefully) never happens? It’s not as exciting as investments or as inspirational as goal-setting, but it’s still a critical item on your financial to-do list.

If you are a sports fan, you know the saying “defense wins championships.” Well, in the financial planning world, insurance = defense and championships = a happy and successful journey.

Key Takeaways

- Physicians should consider the following kinds of insurance: health insurance, life insurance, disability insurance, homeowners or renters insurance, auto insurance, and umbrella insurance. Health, disability, and life insurance are the most important!

- Health insurance is a must, no matter your age! HSAs offer a triple tax advantage — and don’t forget the dental and vision insurance, too!

- Life insurance isn’t necessarily about protecting you; it’s about protecting your family and loved ones after you pass away.

- Probably the most important thing you want to insure is your income. Disability insurance covers you in the event you can’t perform your job, and it usually covers 60% of your income.

- Umbrella policies add another layer of liability protection and are a relatively cheap option to cover your net worth.

Prefer video over the blog? We’ve got you covered! Watch our YouTube video as we dissect this blog post for you:

Why Plan for Insurance?

For physicians, it’s way too easy to be led astray by unscrupulous insurance salesmen into purchasing too much (or sometimes too little) insurance coverage.

Once you have a solid understanding of your cash flow situation, you’re working on paying down debt like student loans, and your emergency fund is looking good, the next step is to turn your focus to risk management and insurance planning.

Risk management and insurance are essential components of financial preparedness because they help mitigate risk. Whether you experience an accident or natural disaster, become disabled, or even pass away, the right insurance coverage can help ensure that you and your family remain protected.

Here are the main types of insurance you should consider as a physician, along with what you should look for in a policy.

Health Insurance

Health insurance is a must-have coverage for any physician—but you already knew that, right?

Even if you’re currently young and healthy, you need coverage to keep you in tip-top shape and safeguard against any significant disasters. If you want to avoid high premiums, it’s a good idea to look into a high deductible health plan (more on this in a moment).

In most cases, your employer provides health insurance as part of your benefits package. If you’re self-employed, however, you may need to purchase health insurance through the marketplace or a private company.

Why should you prioritize a high-deductible health plan? Because these plans are the gateway to one of the most powerful (and secret 🤫) long-term savings vehicles, an HSA.

Health Savings Accounts

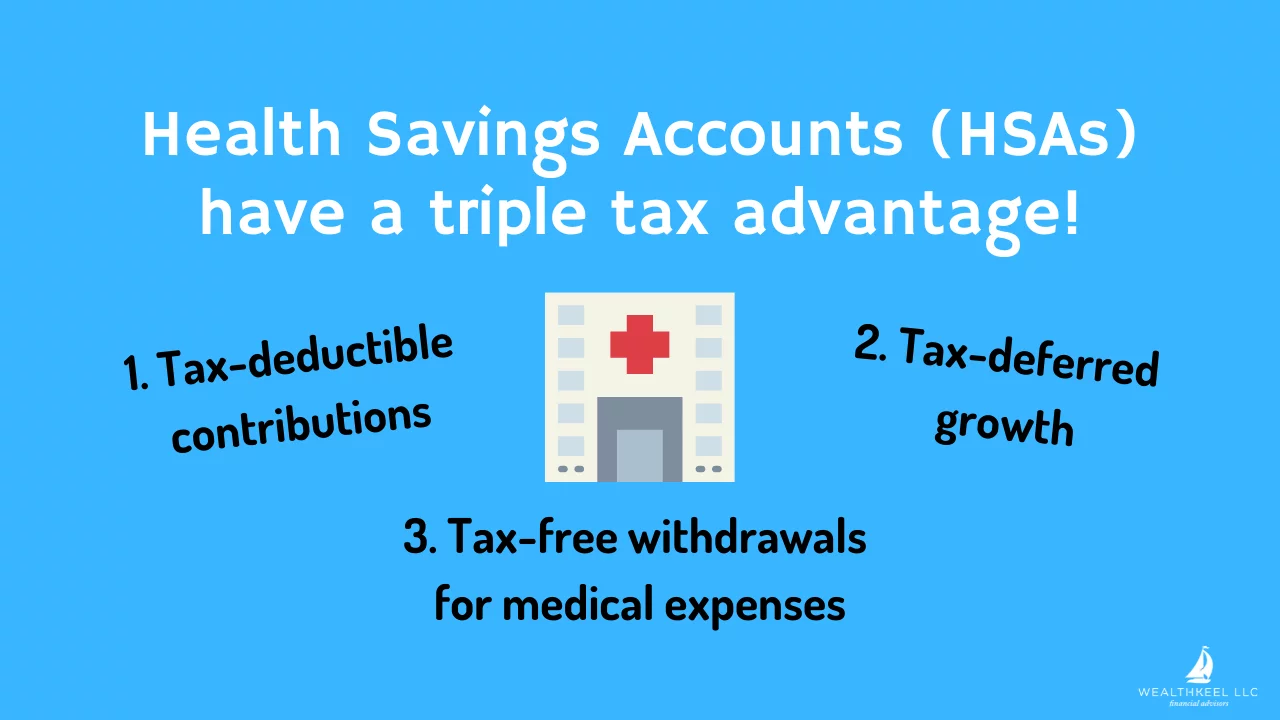

Health Savings Accounts (HSA) are a great way to save money for medical expenses while reaping unparalleled tax benefits. An HSA is a savings vehicle specifically designed to cover medical costs — everything from over-the-counter medicine to surgery to long-term care could qualify.

What makes these accounts so special? The triple tax benefit.

- HSA contributions are pre-tax, so contributing can help lower your annual taxable income.

- Investment earnings grow tax-free—happy dance for more tax-free compounding.

- Distributions for qualified medical expenses remain tax-free.

If you’re looking for a long-term savings unicorn, you’ve found it. An HSA doesn’t have a ‘use it or lose it’ policy like a flexible spending account (FSA). Instead, your HSA account balance rolls over year to year, further promoting its long-term benefits.

These accounts are typically only available for individuals enrolled in high deductible health plans, hence why you should consider one. In 2025, you can contribute up to $4,300 for self-coverage and $8,550 for family coverage. If possible, it’s great to max out your HSA each year. Medical costs in retirement are no joke, and if you want to retire early, you’ll likely need a larger health spending cushion.

Dental and Vision Insurance

Taking care of your teeth and eyes usually isn’t all that hard to do with annual check-ups. You should have access to dental and vision plans via your employer, but you typically have to opt-in.

Many plans offer different tiers of coverage depending on what you need. Luckily, both policies are known for being relatively affordable.

While nearly all employer-sponsored health plans have dental and vision options, some may not. If you don’t have dental insurance and don’t want to sign up for a plan, Dental Savings Plans are another option. These plans are an excellent alternative for dental coverage (just make sure your dentist participates).

Life Insurance

It’s a complete myth that young doctors don’t need life insurance — though it’s certainly an easy one to buy into. You’re young, healthy, and hungry for new experiences. Why on earth should you spend good money each month on a policy you hopefully won’t need for a long, long time?

Here’s the thing: life insurance isn’t necessarily about protecting you; it’s about protecting your family and loved ones after you pass away. It can be used for a variety of expenses:

- Funeral costs

- Paying down debt (student loans or mortgage amounts)

- Aid in funding children’s education.

- Livable income for a spouse or dependent as they adjust to life without you

The amount of coverage you’ll want to purchase depends on your income, including the percentage that currently supports your household and your projected future earnings.

Married couples in their 20s and 30s should discuss life insurance as soon as possible to secure adequate coverage in the event of either spouse’s death. These conversations become especially critical if you have kids. Your and your family’s needs will likely change as your income grows, you purchase a house, start to think about your children’s futures, retirement, and more.

- What do you really want your life insurance policy to cover?

- How much money would keep your family afloat?

- Can the policy help pay off significant debt like a mortgage or student loans?

If you’re single, you may still want to consider carrying a small policy that will cover your funeral expenses if you pass away. Doing so ensures that your relatives and loved ones don’t have to foot the bill on their own if something happens to you. Even if you aren’t interested in purchasing a separate term policy, most companies provide basic life insurance for little to no cost. Contact your HR department to understand your options better.

Term Insurance vs. Whole Insurance: What’s the Difference?

You can obtain two basic types of life insurance policies: term life insurance and whole life insurance. While the right insurance policy for you depends on your particular situation, term life insurance is often a good fit for most.

Why? Mainly because it’s cheap.

Term policies are pretty cost-effective, so it may only set you back one avocado toast or so per month. Let’s take a closer look at each type of policy.

Term Life Insurance

Term life insurance is paid out if the death of a person occurs within the time frame of the policy, usually somewhere between one to thirty years. Most term life insurance is a level term, which means that the death benefit stays the same throughout the policy’s duration.

For example, if you’re 30 years old and purchase a 30-year life insurance policy, the policy will cover you if you pass away anytime from age 30 to age 60. With a level term policy, if the death benefit is $500,000 on day one, it remains $500,000 until the end of the term.

For healthy people, term policies are really affordable. According to Nerd Wallet, the average price for term life insurance is about $26 a month. But keep in mind the price for premiums varies on your age, occupation, health history, and habits/hobbies, and how much insurance you are applying for, among other variables.

Whole Life Insurance

A whole life insurance policy is more comprehensive. It offers permanent death benefit coverage for your beneficiaries, and many also contain a cash-value component that can provide additional tax benefits.

Premiums for whole coverage are much steeper than term policies and may vary throughout the policy. But there are quite a few variations in scope, so make sure you get the one that’s right for you.

Understanding all the ins and outs of your coverage may seem complicated, but it’s worth looking into so you completely comprehend what you get for your money.

Which One is Better?

There’s no one-size-fits-all recommendation when it comes to life insurance policies. Which type of life insurance is best for you depends on various factors, including your age, income, marital status, and whether or not you have any dependents.

While there can be a compelling argument for whole life insurance given the right circumstances like sophisticated estate planning and investment strategies, it certainly isn’t suitable for everyone. Whole life policies tend to be much more complex, so make sure you truly understand every element (including the fine print) before signing.

For most, we often recommend term life insurance. Term life insurance is less expensive since 98% of term policies are never used. For example, a 20 or 30-year term insurance policy for $1,000,000 in coverage can range from $40 to $80 a month for young, healthy professionals. That premium will almost always be much less than the premium from any permanent life insurance policy.

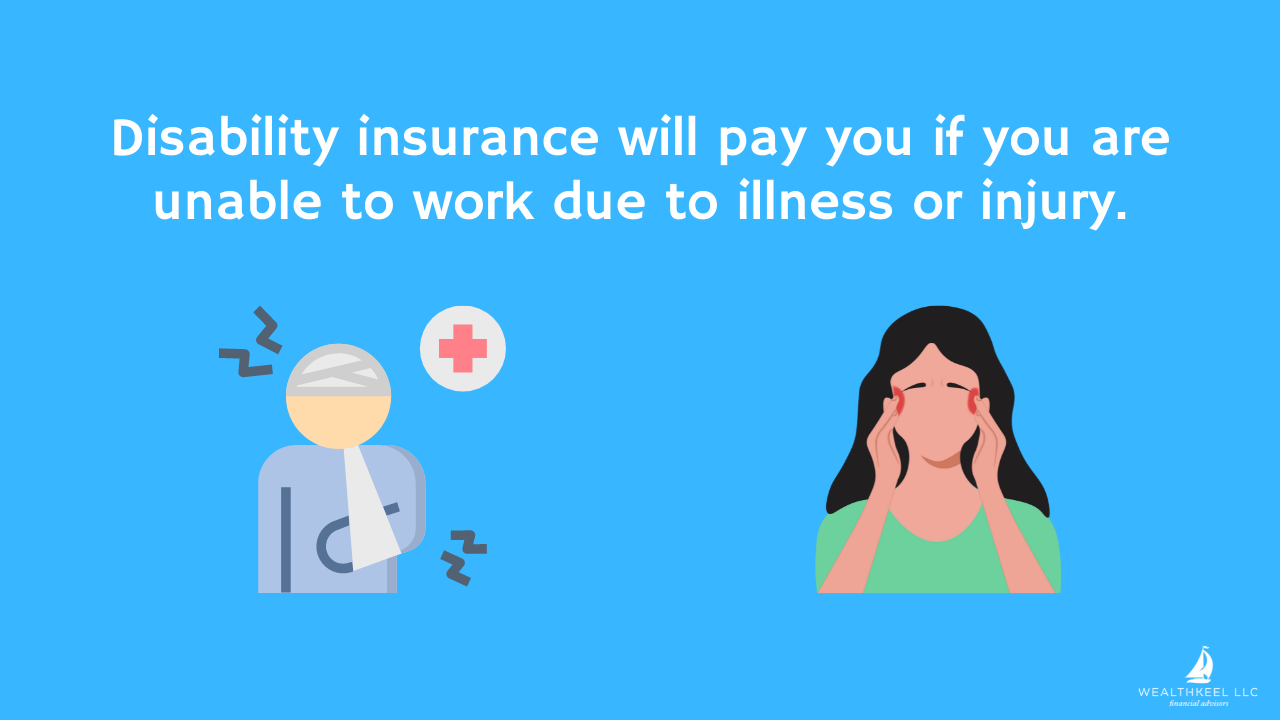

Disability Insurance

What’s the one asset that would be the most difficult to lose?

Your income.

Imagine an injury that prohibited you from doing your job for months. What would you do?

This is where disability insurance comes into play.

Disability insurance is another crucial component of your financial plan. This type of insurance protects your income today and for the rest of your working years.

After 12+ years of medical school and residency/fellowship and a boatload of student loans, what would happen to your earning potential if you become disabled? Without disability insurance, it could be a substantial financial blow to you and anyone else who relies on your income.

Did You Know: Disability insurance is also helpful if you have private student loans since some private lenders will still require payment even if you become disabled. Read your promissory note!

What to Look for in a Disability Insurance Policy

Usually, your hospital for residency or fellowship should offer some type of group disability insurance coverage. This may include short-term disability and long-term disability. Short-term disability covers you immediately after you become injured or disabled and typically lasts for three to six months. Long-term disability replaces your income if you’re no longer working and can last anywhere from two to ten years or even for life.

For example, a typical disability insurance policy might cover 60% of your income up to $20,000/month. If available, take advantage of an employer-sponsored plan since they often secure group rates that are usually cheaper than a private policy. If necessary, search the private market for a disability insurance policy to supplement what you already have from your employer.

You should also check whether you’re eligible for any discounts or unisex rates through your hospital. If you have enough people from one hospital that purchase disability insurance, insurers will often provide discounted rates and/or unisex rates. Unisex rates are essential for women because their premiums are usually higher.

Pro-Tip: If you are a female physician or male physician with less than average health, and you are still in training, ask your HR if you have a GSI (Guaranteed Standard Issue) policy available for you. This can lock in unisex rates, which will save females a lot of money in premiums. Also, if you have some blemishes on your medical history, a GSI will have little to no underwriting, assuming you have not been declined in the past. Fun bonus facts for unisex plans; In Montana, all policies have unisex rates, In Massachusetts (Bill H.482), some insurance companies offer unisex rates, and Ameritas also provides unisex rates for all policies issued with a discount in Ohio.

Disability Insurance Riders

There are several different riders you may be able to add to your policy. Still, you shouldn’t let an insurance agent upsell you on every possible rider without understanding the specifics of each benefit. Most riders will increase your premium and, subsequently, the insurance agent’s commission.

First, look for a non-cancelable/guaranteed renewable policy. You also want to look for an own-occupation policy, sometimes labeled as “specialty-specific” or “tier 3 coverage”, which ensures that you’ll still be eligible for disability benefits even if you begin a new career in a different field. For example, if you’re a surgeon but can no longer perform surgery, you will still be paid even if you can become a professor earning six figures.

Pro-Tip: There are only five companies that offer this definition of Total Disability to physicians, including Berkshire Life (a Guardian Company), Standard Insurance Company, Principal, Ameritas, and MassMutual – AKA The Big Five

Other notable riders include residual disability and cost of living, and catastrophic coverage, which is usually inexpensive and worth it. If you are a young physician with many pay increases ahead of you, make sure your policy has a guaranteed future purchase option. This rider will allow you to increase your insurance benefit amount by showing your increased pay via tax documents or pay stubs without having to answer any medical questions or prove insurability.

Homeowners or Renters Insurance

Home insurance and renters insurance protect your property and personal possessions in the case of an accident, theft, or natural disaster. For example, if your apartment burns down and your possessions are damaged or destroyed, renters insurance would cover the cost of your possessions.

Personal Property Coverage

Personal property coverage covers damage to your personal belongings in a homeowners insurance or renters insurance policy. This includes items like clothing, electronics, furniture, and more. You may also want to purchase additional coverage for expensive items like jewelry or fine art.

Liability Coverage

When shopping for homeowners’ or renters’ insurance, it’s also important to secure good liability coverage. Liability insurance protects you in case anything happens to a guest or visitor on your property. The minimum coverage for a homeowners insurance policy is $500,000 in liability protection.

Dwelling Coverage

While dwelling coverage doesn’t apply to renters insurance policies, it’s an essential component of an effective homeowners insurance policy. Dwelling coverage covers damage to the structure of your home, including your walls, roof, and foundation.

Auto Insurance

Car insurance is required in almost all states if you own a vehicle. When shopping around for an auto insurance policy, it’s crucial to compare rates from multiple providers to ensure you’re getting the best rate possible. Even if you’re happy with your current coverage, it’s wise to regularly reevaluate your auto insurance policy to score the best deals. This is especially true if you’re a younger driver since age is a significant factor contributing to your premiums.

Collision and Comprehensive Coverage

When purchasing an auto insurance policy, there are typically minimum coverage requirements depending on your state. While collision and comprehensive coverage aren’t usually required, they’re almost always a good idea. Collision coverage covers the cost of repairing your vehicle if you get into an accident. Comprehensive coverage covers the cost of repairs if anything else happens to your car, like theft or weather damage.

Umbrella Insurance

Once your assets surpass your current liability coverage, it’s usually a good idea to add an umbrella policy. Truthfully, every physician should have an umbrella policy. Umbrella policies add another layer of liability protection and are relatively cheap. You should look for a $1 million policy to start, and then increase with your net worth. If you spend a lot of time on the road or have guests over frequently, you may want to purchase umbrella insurance coverage even before you’ve exhausted your other policies.

Pro-Tip: Your umbrella coverage should always cover your net worth and always round up to the next million since this insurance is very cost-effective. For many, a $1,000,000 policy should cost around $250 per YEAR.

How to Purchase Insurance as a Physician

Many insurance companies and salespeople sell to young physicians, but they may convince you to buy more insurance than you truly need. Before you purchase any insurance policy, ensure you do your research and consider several options.

It’s also a good idea to call another advisor, ask their opinion, and check out sites like The White Coat Investor. Not only can you see what other medical professionals are saying, but you can also see what other financial professionals recommend.

While it’s essential to be appropriately insured, you may not need every type of insurance on this list. For instance, you may not need to pay for permanent life insurance, which is usually much more expensive than term life insurance. The right coverage for you depends on your age, family, health, assets, debts, lifestyle, and more.

Along with malpractice insurance, you should make sure you review all the insurances above and add the appropriate risk management for you and your family.

You Have Insurance, Now What?

Once you’re properly insured, there are a few steps you should take to cement your financial wellbeing and prepare for the future: take action to prevent identity theft and prepare estate documents.

Identity Theft Protection

While not a type of insurance, identity theft protection is almost as important when it comes to protecting your financial health. To avoid becoming a victim of identity theft, you should annually review your credit reports. It’s free to access, and some financial institutions even offer free ongoing credit monitoring.

The main credit bureaus you should keep an eye on are Experian, TransUnion, and Equifax. Your score will likely be slightly different across these three platforms, which is normal. When reviewing your report, you look for any unauthorized accounts or other errors affecting your score.

Your credit score remains a critical indicator of your long-term financial health. Banks and other lenders use those precious three numbers for qualifications on loans like a mortgage, car, or personal loan. You can build up your credit by not overspending, paying your bills consistently on time, and keeping an eye on identity protection.

Get Your Estate Documents in Order

Estate planning, yet another financial chore that has to do with death. While proper estate planning is an important component of financial preparedness, over 60% of Americans don’t even have a will in place. Even younger physicians should plan and get their estate in order as soon as possible.

You should visit your local Estate Planning attorney and have the following documents completed:

- Will

- Living Will

- Health Care Power of Attorney

- Financial Power of Attorney

While the costs can vary from attorney to attorney and from city to city, the process isn’t costly; an individual may spend $1,000-$2,000 (depending on a few factors, but that should be a fair range), which is well worth it when it comes to your peace of mind.

Putting It All Together

Proper insurance coverage is a critical component of any solid financial plan. While it may not seem as urgent as paying down debt or saving for retirement, comprehensive insurance coverage can help protect you and your family in the event of the unexpected.

When shopping for insurance coverage, evaluate all of your options before making a decision. You shouldn’t take advice from a “financial planner” who may be an insurance salesperson hiding behind a misleading title. How will you know the difference? Look for insurance advice from a fee-only fiduciary advisor, so you can be confident their recommendations aren’t tied to a commission check.

Many physicians are high-earners and, as such, require the proper protection. The three most important policies to carry are (aside from Malpractice!):

- Health insurance

- Disability insurance

- Life insurance

These policies will help to ensure that you and your family can weather whatever life throws at you. Because physicians are often in a unique financial position relative to the average American, ensuring a steady income for you and your family in the case of an injury, disability, or even death is a healthy long-term approach.

Looking for a more thorough all-in-one spot for your financial life? Check out of free eBook, A Doctor’s Prescription to Comprehensive Financial Wellness.